2. Inward Bill Collection (DA/DP)

The Bank will save time and collect your goods quickly with the Inward Bill Collection facilities. The banks will help process these documents and payments on your behalf. There are two ways the bills are being collected:

i. Documents against Acceptance (DA) The Bank will release the import documents to you upon acceptance of the bills of exchange/drafts; and you have an agreement to pay the seller a certain amount on a predetermined date.

ii. Documents against Payment (DP) The bank will release the import document to you upon your payment.

3. Shipping Guarantee

Shipping Guarantees are formal financial obligations or undertakings in favour of third parties, issued by banks on behalf of customers, to facilitate their business dealings

1. Help reduce the risk associated with global trade

Trade finance can help reduce the risk associated with global trade by reconciling the divergent needs of an exporter and importer. Ideally, an exporter would prefer the importer to pay upfront for an export shipment to avoid the risk that, the importer takes the shipment but refuses to pay for the goods. However, if the importer pays the exporter upfront, the exporter may accept the payment but refuse to ship the goods.

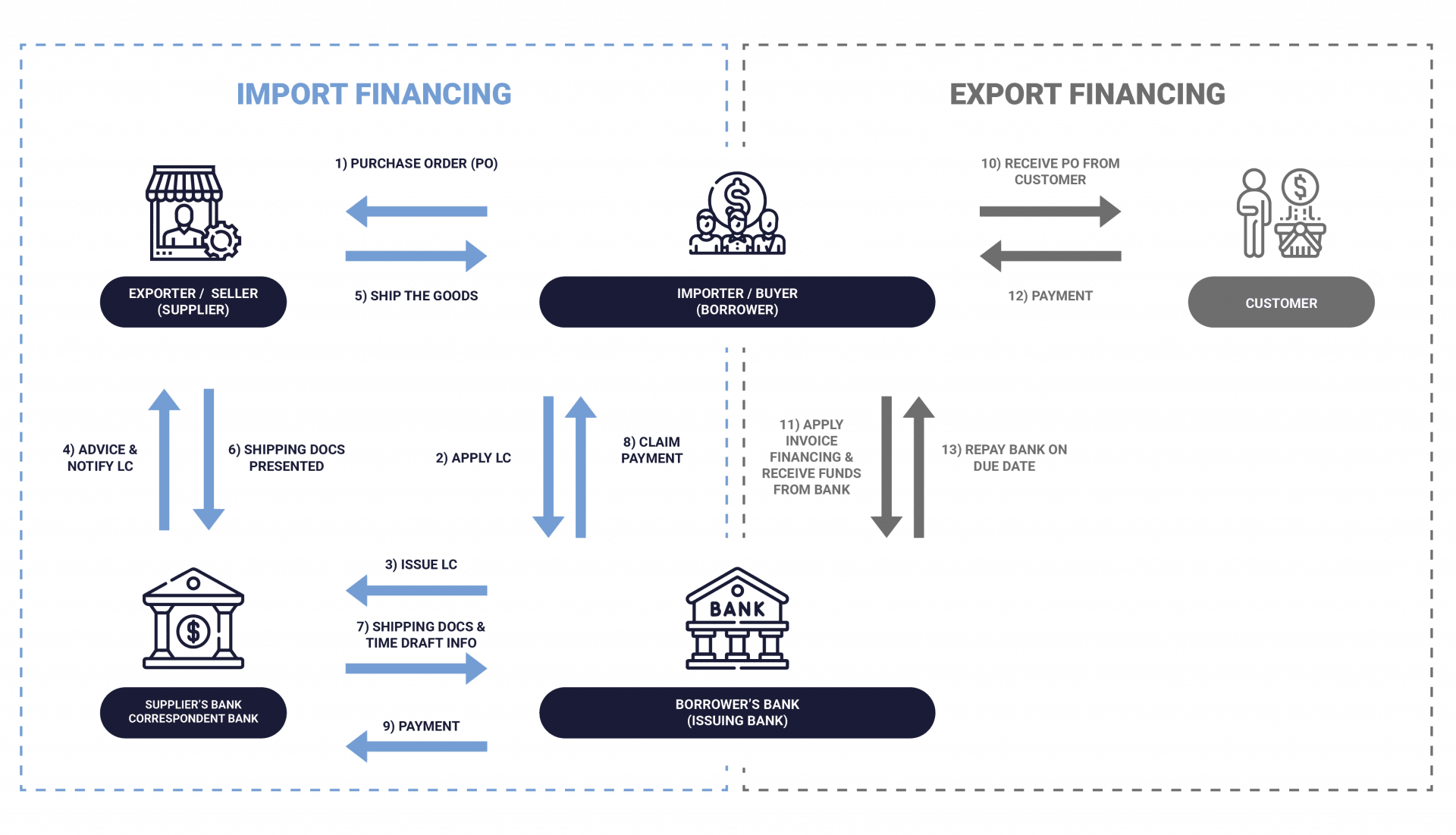

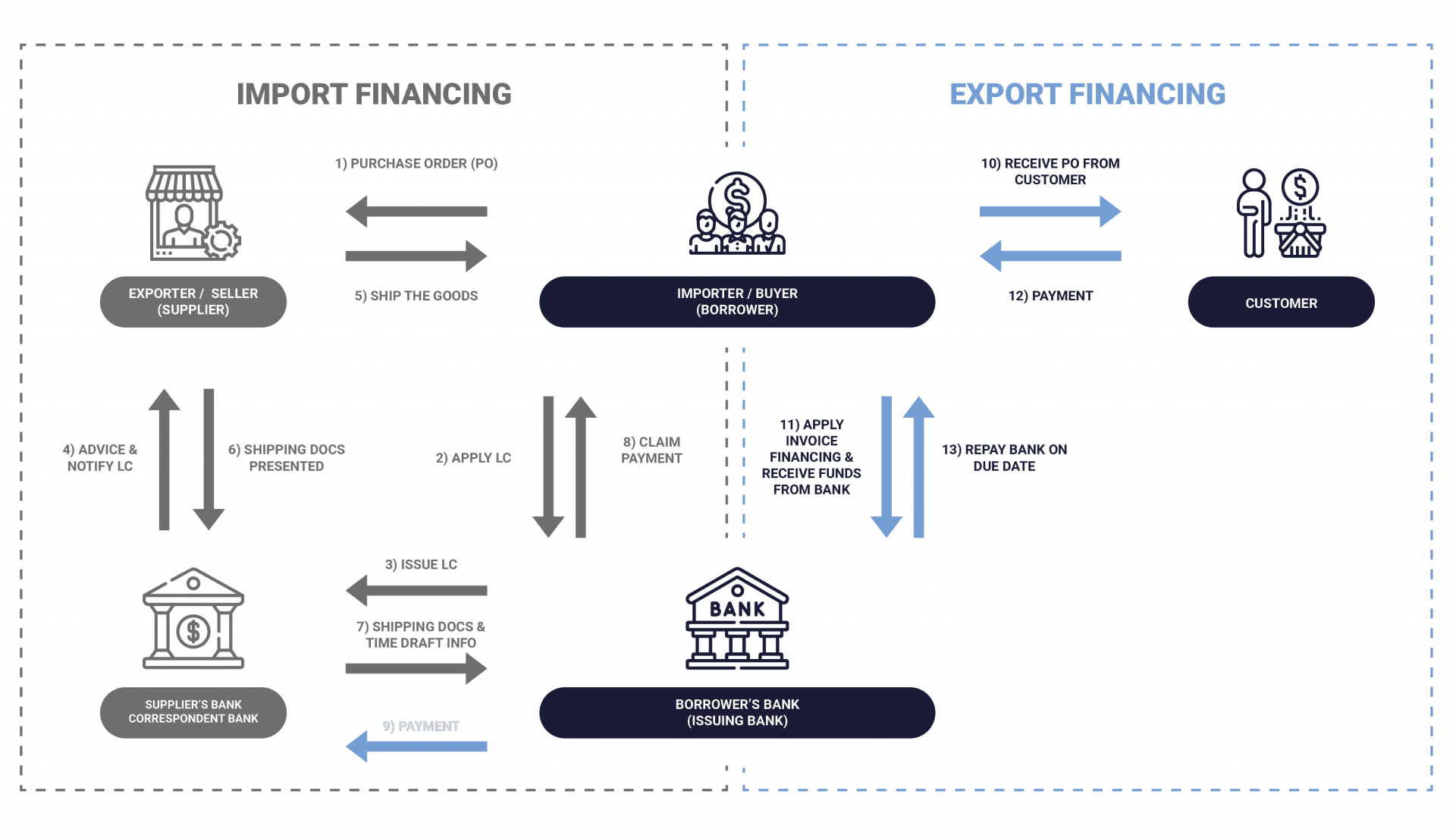

A common solution to this problem is for the importer’s bank to provide a letter of credit to the exporter's bank that provides for payment once the exporter presents documents that prove the shipment occurred, like a bill of lading. The letter of credit guarantees that once the issuing bank receives proof that the exporter shipped the goods and the terms of the agreement have been met, it will issue the payment to the exporter.

With the letter of credit, the buyer's bank will take on the responsibility of paying the seller. The buyer's bank would have to ensure the buyer was financially viable enough to honor the transaction. Trade finance helps both importers and exporters build trust in dealing with each other and thus facilitating trade. Trade finance allows both importers and exporters to access to many financial solutions that can be tailored to their situation, and sometimes, multiple products can be used to help ensure the transaction goes through smoothly.

2. Improves Cash Flow and Efficiency of Operations

Besides reducing the risk of non-payment and non-receipt of goods, trade finance has become an important tool for companies to improve their efficiency and boost revenue.

It is an extension of credit in many cases. Trade finance allows companies to receive a cash payment based on accounts receivables in case of factoring. A letter of credit might help the importer and exporter to enter a trade transaction and reduce the risk of non-payment or non receipt of goods. As a result, cash flow will be improved since the buyer's bank guarantees payment, and the importer knows the goods will be shipped.

In other words, trade finance ensures fewer delays in payments and allows both importers and exporters to run their businesses and plan their cash flow more efficiently.

3. Increased Revenue and Earnings

Trade finance allows companies to increase their business and revenue through trade. For example, a company that can clinch a sale for a large order, might not have the ability to produce the goods needed for the order.

However, through the help of trade financing from the banks, the exporter can complete the order by having the financial means to pay their suppliers.

As a result, the company gets new business that it might not have had, with the support that trade finance provides.

4. Reduce the Risk of Financial Hardship

Without trade financing, a company might fall behind on payments and lose a key customer or supplier that could have long-term impact for the company. Having options like revolving credit facilities and accounts receivables factoring can help companies on their cashflow and tie them through in times of financial difficulties.